Competitive analysis: Porter’s five forces model

How can competitive analysis: porter’s five forces model support strategic choice or positioning?

Contents

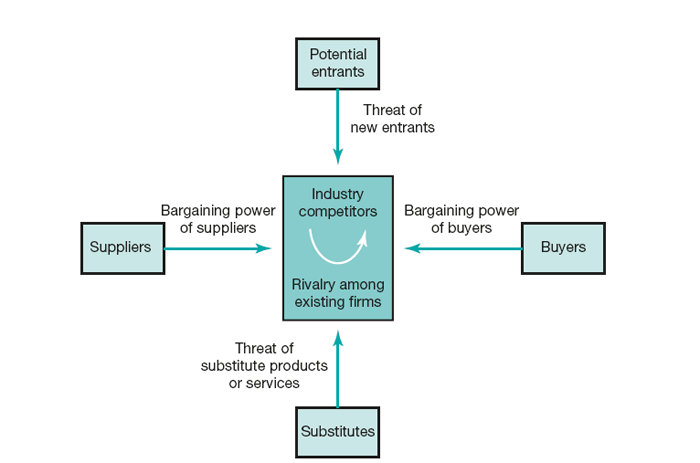

Porter’s (1980) competitive analysis identifies five fundamental competitive forces that determine the relative attractiveness of an industry: new entrants, bargaining.

Porter’s Five Forces framework analyses the structural pressures that determine how economic value is divided within an industry: rivalry, new entrants, substitutes, buyer power and supplier power. Weaker forces generally support higher long-run profit potential. The analysis helps a company understand industry economics, choose a defensible position and identify structural changes it can influence.

When to use it

Use the framework to understand an existing industry, test entry into a new one or evaluate the attractiveness of a segment. It expands analysis beyond direct rivals to customers, suppliers, substitutes and potential entrants. Repeat it when technology, regulation, consolidation or a business-model shift changes the industry boundary or economics.

Origins

Michael E. Porter introduced the framework in his late-nineteen-seventies Harvard Business Review article “How Competitive Forces Shape Strategy” and developed it in the 1980 book Competitive Strategy. Drawing on industrial-organisation economics, he moved analysis beyond rivalry to five structural forces that allocate value among industry participants. The framework explains differences in long-run profitability and helps firms locate positions where forces are weaker or can be shaped.

What it is

The five forces are rivalry among existing competitors, threat of entry, threat of substitutes, bargaining power of buyers and bargaining power of suppliers. Each has specific drivers. A useful analysis explains who captures value, why the pressure exists and how it is likely to change rather than assigning unsupported high, medium or low labels.

How to use it

Define the industry by product or service, customer need, geography and value-chain scope. State the time horizon and gather evidence from customers, suppliers, competitors, financial data and regulation. Then analyse the strength, direction and drivers of each force.

1. New entrants

Assess whether attractive profit can draw new capacity into the industry and what protects incumbents:

- Economies of scale and network effects raise the volume required for efficient entry.

- Established brands and loyalty, such as Coca-Cola’s, increase acquisition cost.

- Large, risky up-front capital requirements deter entry.

- Customer switching costs protect incumbents when they are meaningful and durable.

- Restricted or costly distribution access creates a barrier.

- Patents, licences, know-how, advantaged inputs, assets, experience or subsidies can create scale-independent cost advantages.

- Regulation may require scarce operating licences, as in wireless spectrum.

- Credible retaliation deters entry; expected passivity encourages it.

- High margins can attract entry unless barriers protect them; an entry-deterring price reduces that invitation.

2. Substitutes

Identify different products or services that satisfy the same underlying need. A bus can substitute for a train even though the technologies differ. Threat rises when the alternative offers a better price–performance trade-off, has low switching cost or benefits from a favourable trend. Discuss the customer’s job, not only the current category.

3. Buyers’ bargaining power

Assess buyers’ ability to force prices down, demand more service or shift cost and risk:

- High-volume or concentrated buyers can demand better terms; large grocery retailers often pay less than small stores.

- Buyers negotiate harder when the purchase represents a large share of their cost.

- Undifferentiated offers and low switching costs make suppliers easier to play against one another.

- Low-margin buyers face strong pressure to reduce input cost.

- Credible backward integration or partial in-house production strengthens bargaining and reveals supplier economics.

- Buyers are more price-sensitive when the input has little effect on their own performance.

- Better information about prices, costs and alternatives increases buyer leverage.

4. Suppliers’ command of industry

Supplier power mirrors buyer power and determines how much value input providers can capture:

- Concentrated suppliers serving fragmented buyers have more influence.

- A lack of alternative inputs limits buyer choice.

- Suppliers with attractive alternative customers, industries or channels can walk away more easily.

- An indispensable or high-impact input increases dependence.

- High switching cost or stranded assets strengthen the incumbent supplier.

- A credible threat of forward integration into the buyer’s customer market adds leverage.

5. Existing competitors

Rivalry appears through pricing, promotion, innovation, service and competition for customers or channels. Escalating price moves can destroy profit for every participant, while advertising or innovation may expand demand or sharpen differentiation. Rivalry intensifies when:

- competitors are numerous or similar in strength;

- industry growth is slow, so share must be taken rather than absorbed by expansion;

- high fixed cost or perishable capacity encourages volume and price competition;

- commodity-like offers and low switching costs make price decisive;

- diverse strategies and ownership make responses hard to predict;

- strategic stakes are high, as when establishing a customer base in communications or online markets; and

- specialised assets, labour commitments, closure costs, emotional attachment or strategic dependencies create high exit barriers.

Summarise the forces in economic terms, identify which drivers matter most and develop strategic responses: position in a less exposed segment, differentiate, alter switching costs, redesign make-or-buy choices or shape industry structure lawfully. Define leading indicators and refresh the analysis.

Final analysis

Five Forces explains external structure more directly than the internal capabilities required to exploit a position. Combine it with an inside-out resource and capability analysis. This prevents a structurally attractive opportunity from being mistaken for one the organisation can actually win.

Government, partners and complementors are sometimes proposed as extra forces. They are important, but often affect profitability through entry, rivalry, substitutes or bargaining power. Model them separately when doing so reveals a genuinely distinct mechanism; do not add boxes merely to make the diagram look comprehensive.

Top practical tip

For every force, identify the two or three economic drivers that matter most, the evidence for them and the leading indicator that would show the structure changing.

Top pitfall

Define the industry carefully and do not turn the framework into a static checklist. A boundary drawn too broadly or narrowly changes every force, while technology, regulation, complementors, and business-model change can alter the structure faster than a one-time analysis suggests.

Further reading

Porter, M.E. “How competitive forces shape strategy.” Harvard Business Review.

Porter, M.E. (1980,1998) Competitive Strategy: Techniques for Analyzing Industries and Competitors. New York: Free Press.

Harvard Business School Institute for Strategy and Competitiveness, “The Five Forces”.