Discounted cash flow (DCF) and net present value (NPV)

How can discounted cash flow (dcf) and net present value (npv) support strategic choice or positioning?

Contents

Discounted cash flow (DCF) is a method to assess and compare the current and future values of an asset.

Discounted cash flow, or DCF, converts expected future cash flows into today’s value. Net present value, or NPV, adds the discounted inflows and outflows associated with an investment. Together they allow decision makers to compare the capital committed now with the value expected later, after accounting for time and risk.

When to use it

Use DCF and NPV in capital budgeting and investment appraisal to decide:

- which projects should be accepted;

- how much capital expenditure the firm should undertake;

- how a selected portfolio should be financed.

Include only relevant incremental cash flows—future cash flows that differ among alternatives. The discount rate should reflect the time value of money and the risk of the forecast cash flows. A positive NPV indicates that the project is expected to earn more than the selected required return, given the assumptions.

Origins

Present-value reasoning grew from centuries of interest and annuity calculation, with industrial applications appearing by the early nineteenth century. Irving Fisher provided the modern economic foundation for intertemporal value in The Theory of Interest. John Burr Williams applied discounted future cash flow to investment valuation in The Theory of Investment Value, published in nineteen thirty-eight. NPV later became a standard corporate-finance rule for comparing discounted project inflows and outflows.

What it is

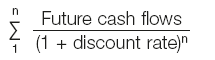

DCF discounts each expected cash flow according to when it occurs and the return required for its risk. NPV is the total of those present values, including the initial investment: NPV = Σ CFₜ/(one + r)ᵗ. A result above zero supports investment on financial grounds; a result below zero suggests the forecast return does not meet the hurdle rate. The arithmetic is mechanical, but cash-flow, terminal-value and discount-rate assumptions require judgement.

How to use it

First forecast the incremental cash inflows and outflows over an explicit horizon. Exclude sunk costs, include opportunity costs and model working capital, tax and terminal value consistently.

Discount each cash flow with the selected rate:

Build the rate from a basis appropriate to the cash flows. A risk-free component compensates for deferring consumption and reflects the time value of money. A risk premium compensates for uncertainty that the forecast cash will not materialise. In corporate appraisal, a weighted average cost of capital or another opportunity-cost measure may be more appropriate than simply adding an arbitrary premium.

Sum all discounted inflows and outflows to obtain NPV, then compare the result with competing projects and capital constraints. Keep nominal cash flows with a nominal discount rate and real cash flows with a real rate. Test the assumptions through scenarios and sensitivity analysis.

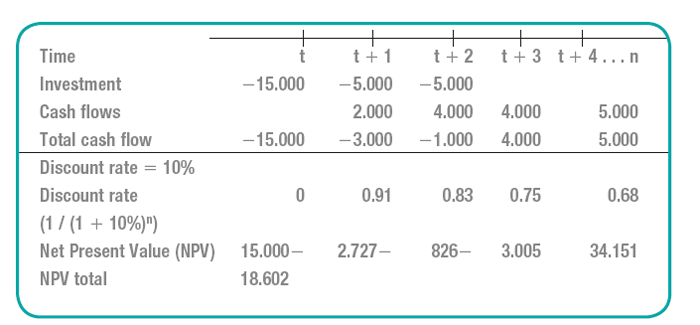

The worked example below illustrates the calculation:

Final analysis

John Burr Williams published the investment-valuation framework in 1938, and DCF and NPV subsequently became standard tools throughout finance.

Their power can create false confidence. Small changes in growth, margin, terminal value or discount rate may cause large valuation changes. Forecast cash flows received after 5 or 10 years are especially uncertain. The responsible output is therefore a valuation range with explicit drivers, not one precise point estimate. Related approaches such as WACC can improve consistency in the required-return assumption, but cannot remove forecast uncertainty.

Top practical tip

Build the model from operating drivers and incremental cash flows, then show how value changes under credible downside, base and upside assumptions. Make the discount rate, terminal value and timing conventions easy to inspect.

Top pitfall

Do not use the discount rate as a hidden plug to force the desired answer. It must match the risk and currency of the cash flows. A sophisticated spreadsheet cannot compensate for implausible volume, margin or terminal assumptions.

Further reading

Brealey, R.A. and Myers, S.C. (2003) Principles of Corporate Finance, 7th edition. London: McGraw-Hill.

Walsh, C. (2008) Key Management Ratios: the 100+ Ratios every Manager Needs to Know. Harlow: Pearson.

Willams, J.B. (1938) Theory of Investment Value, Cambridge: Harvard University Press.