Overhead value analysis

How can overhead value analysis improve people, teams, or organisational effectiveness?

Contents

Overhead value analysis (OVA) is a technique used to find opportunities to reduce overhead costs.

Overhead value analysis (OVA) examines the cost and value of indirect activities and services. It makes support work visible, asks internal customers what outputs they actually require and identifies opportunities to eliminate, simplify, automate, integrate, decentralise or outsource activities. The objective is to improve the value of overhead—not to assume that every indirect cost is waste.

When to use it

Use OVA when overhead has grown without a clear link to organisational priorities, when support services no longer meet internal-customer needs, or when financial pressure requires a disciplined redesign. It can be preventive or corrective. Because the analysis may affect roles, workload and employment, establish transparent decision criteria, worker consultation and implementation support at the outset.

An example OVA project

A manufacturer of military and advanced remote-control technology faced deteriorating financial results and limited organisational adaptability. Its OVA team created a structured inventory of indirect activities and costs, then used a full analysis to redesign support work. The organisation shifted from a functional structure toward market-facing business units. Departments clarified the value delivered to internal customers, while selected activities were decentralised. Broad participation helped employees shape the change rather than experience it only as a cost-cutting exercise. This example illustrates a possible route, not proof that the same structural response fits every organisation.

Origins

OVA belongs to the wider value-analysis and value-engineering tradition, which asks whether an activity or component performs its required function at an appropriate cost. Its management-accounting form combines that logic with activity-based costing, internal-customer evaluation and Porter’s value-chain perspective. The cited literature documents these related streams rather than establishing one definitive inventor of OVA.

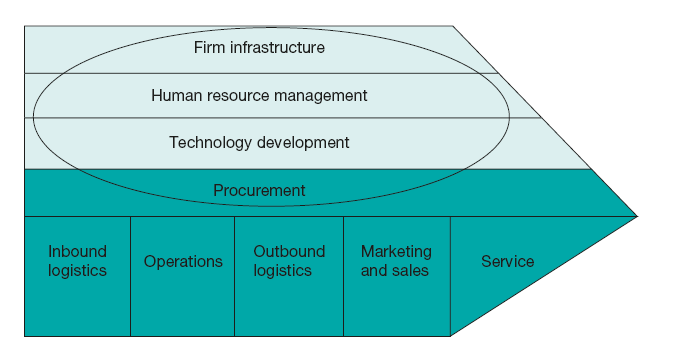

What it is

OVA compares the resources consumed by indirect activities with the services and outcomes required by primary processes. Porter’s value chain helps locate support activities, while activity-based costing helps trace resource consumption. Interviews and questionnaires add judgments about necessity, quantity and quality that accounting records cannot supply on their own.

How to use it

Use six connected steps. Keep the evidence trail from requested output through activity and cost to the proposed change.

| 1 | Create the foundation. Define the scope, organisational objectives, customers, required outputs and criteria for assessing each output. Distinguish mandatory controls from discretionary services before discussing reduction. | |

|---|---|---|

| 2 | List activities and costs systematically. Identify resources, activities and outputs, then assign costs to products or services, commonly with activity-based costing (ABC). Record assumptions instead of presenting uncertain allocations as facts. | |

| 3 | Evaluate with customers. Ask internal customers whether each service is critical, desired or merely nice to have, and assess its quality, quantity and cost. Use interviews and questionnaires, then compare stated preferences with operational, legal and risk requirements. | |

| 4 | In step 4, identify improvement opportunities. Translate evidence into options to eliminate, change, automate, integrate, decentralise or outsource work. Make the effect on service, control, capacity and employees explicit. | |

| 5 | In step 5, prioritise opportunities using the same evaluation dimensions: | |

| • | Necessity: does the output add required value? | |

| • | Quality: is the output fit for its purpose? | |

| • | Quantity: is the volume appropriate? | |

| • | Cost: can the output be delivered economically? | |

| Prioritisation is a management judgment informed by finance, process expertise and the managers responsible for overhead services. Assess dependencies and implementation risk before combining options. | ||

| 6 | Implement and monitor. Assign owners, consult affected people, sequence the changes and track service, cost, risk and workforce effects. Confirm that savings are realised without moving hidden work into primary teams. |

The success factors of an OVA project are:

- Organisational objectives and non-negotiable obligations are explicit.

- The current structure, accountabilities and process boundaries are understood.

- The scope and cost definitions are agreed before options are scored.

- Dependencies with other projects are coordinated.

- Employees, internal customers and decision-makers have meaningful involvement.

Final analysis

OVA combines quantitative cost information with qualitative judgments about service value. Its apparent precision can therefore be misleading. Cost allocations depend on assumptions, and employees may reasonably be cautious when the analysis could alter or remove their roles. Triangulate interviews, process evidence, workload data, customer experience and relevant benchmarks rather than relying on one source.

The analysis can also shift work instead of removing it: an abolished support activity may reappear as unmeasured administrative effort in frontline teams. Test every proposal for total cost, control effectiveness, service quality, employee impact and implementation capacity. Participation improves both the evidence and the legitimacy of change, but it must be genuine; a predetermined redundancy programme should not be presented as collaborative analysis.

OVA is often paired with activity-based costing (see Activity-based costing), yet neither method decides what the organisation should value. Strategic priorities and stakeholder obligations still govern that choice.

Top practical tip

Create one traceable inventory connecting each overhead activity to its cost, customer, required output and governing obligation. That foundation makes improvement options comparable and exposes work that would otherwise be displaced rather than removed.

Top pitfall

Do not equate “indirect” with “unnecessary.” Poor allocations, employee fear or an exclusive focus on short-term savings can produce false precision, weaken essential controls and transfer hidden work to primary teams.

Further reading

Davis, M.E. and Falcon, W. D. (1964) Value Analysis, Value Engineering: The Implications for Managers. New York: American Management Association

Mowen, M.M. and Hanson, D.R. (2006). Management Accounting: The Cornerstone for Management Decisions. Mason, Ohio: Thomson South-Western.

Porter, M.E. (1985) Competitive Advantage: Creating and Sustaining Superior Performance. New York: Free Press.