Value-based management

How can value-based management support strategic choice or positioning?

Contents

Value-based management (VBM) is a tool for maximising the value of a corporation.

Value-based management (VBM) aligns strategy, resource allocation, performance management and incentives around sustainable economic value creation. Its central test is whether an investment is expected to earn more than the cost of the capital committed to it. Discounted future cash flow provides the valuation logic, while operational value drivers connect that logic to everyday decisions.

When to use it

Use VBM to set goals, evaluate strategy and performance, allocate capital, design incentives, communicate with investors and value businesses or projects. Traditional accounting measures such as earnings per share or return on equity can report profit without charging fully for the opportunity cost of invested capital. VBM makes that charge explicit.

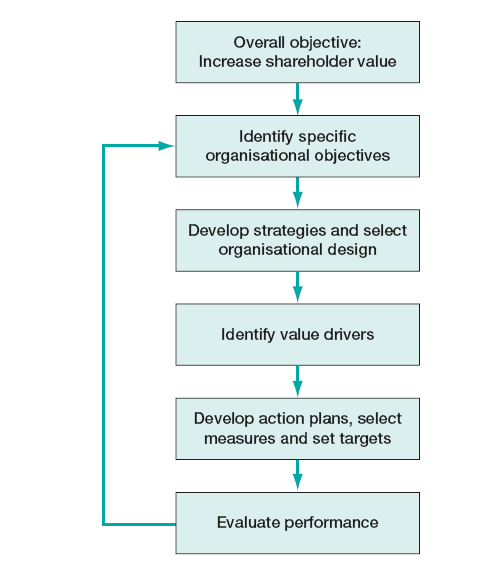

Implementation requires attention to four connected areas:

- Measurement

- Management

- Motivation

- Mindset.

For measurement, define adjustments that translate accounting profit into economic profit, identify accountable VBM centres and connect those centres so local choices support enterprise value. The centres may vary in size, but each needs relevant drivers and responsibility for results.

For management, integrate value drivers into strategy, planning, budgeting and operational review. Calculating value without changing decisions produces a reporting exercise, not a management system.

For motivation, link incentives to value created over an appropriate horizon rather than to negotiating and beating a short-term budget. Managers should share in upside only where the design also addresses risk, underperformance and factors outside their control.

For mindset, build a shared understanding that capital is scarce and has a cost. People need to see how service, pricing, working capital, growth and investment choices affect long-term cash generation.

Origins

VBM developed from corporate-finance work on discounted cash flow, shareholder value and economic profit. Alfred Rappaport connected strategy to shareholder-value analysis, while G. Bennett Stewart helped popularise economic value added. Consulting and finance practice then extended these concepts into integrated systems for planning, performance measurement and incentive design.

What it is

A common VBM measure is economic value added (EVA): operating profit after an appropriate tax treatment less a charge for the capital employed. Unlike return on investment or earnings per share alone, EVA explicitly recognises that equity and debt capital carry an opportunity cost. Weighted average cost of capital supplies a common hurdle rate, while value-driver trees translate the financial outcome into controllable operating factors.

VBM is broader than a single formula. It asks managers to compare strategic options by the present value of expected cash flows, identify assumptions that create or destroy value and allocate resources accordingly.

How to use it

- Start with the strategic decision and its operating value drivers; do not let pursuit of a theoretically exact valuation obscure the practical choice.

- Use only accounting adjustments that materially improve economic interpretation. Excessive complexity weakens understanding and ownership.

- Focus on change in value and the causes of that change rather than treating one absolute valuation as certain.

- Embed VBM in strategic planning, capital allocation, budgeting, review and control instead of running it as a separate finance exercise.

- Secure visible senior-management commitment and give accountable managers the authority and information needed to influence their drivers.

Final analysis

VBM is most valuable as a decision discipline. Forecasts of future cash flow and the selected discount rate are uncertain, so the calculated value is not an objective fact. Use scenarios and sensitivity analysis, make assumptions visible and examine how actions influence value over time.

A narrow shareholder-value interpretation can reward short-term cash extraction while ignoring damage to employees, customers, capabilities or society. Those effects eventually influence cash flow and risk, even when a model initially leaves them outside its boundary. Combine financial value with strategic resilience and material stakeholder consequences.

Top practical tip

Build a short value-driver tree for the decision and assign each driver to an accountable owner. Review how operating choices change future cash flow, capital employed and risk; the conversation is more useful than debating a single valuation decimal.

Top pitfall

A value model is only as credible as its forecasts, discount rate, time horizon and boundary. Do not turn uncertain assumptions into rigid targets or create incentives that sacrifice long-term capability and stakeholder trust for near-term financial appearance.

Further reading

Ittner, C.D. and Larcker, D.F. (2001) “Assessing Empirical Research in Managerial Accounting: A Value-Based Management Perspective.” Journal of Accounting and Economics 32, 349–410.

Rappaport, A. (1986) Creating Shareholder Value: A Guide for Managers and Investors. New York: Simon & Schuster.

Stewart, G.B. (1990) The Quest for Value. New York: HarperCollins.